What If Solving Climate Change Didn’t Require Sacrifice... But Ethos? - Part 3: Life & Lands

Geo-engineering and Planetary Health — Investment Opportunities and Landscape in 2025. We've interviewed one of the family office in our coalition actively investing in the sector. Stay ahead with us!

Introduction

Over the next decade (2025–2035), Geo-engineering and Planetary Health might become two of the most structurally critical—and still vastly undervalued—investment frontiers in global capital markets.

In May 2025, the UK’s Advanced Research and Invention Agency (ARIA) quietly green‑lit “small‑scale outdoor geo‑engineering experiments,” deploying sun‑reflecting particles in the stratosphere and brightening clouds—marking one of the first national approvals for real‑world climate intervention trials.

Meanwhile, Brazil is enduring a historic drought across its Cerrado and Amazon regions, pushing coffee and beef prices sharply higher—coffee futures recently hit record highs and some beef exports rose an estimated 18%.

In response, Brazilian farmers are investing heavily in irrigation & looking at using cloud seeding solutions, signaling an irreversible transformation in agricultural infrastructure.

Across Thailand and Vietnam, late‑2024 floods brought by Typhoon Yagi and a powerful monsoonal surge devastated communities & distrupted the local agriculture infrastructure for at least a decade. In Vietnam, the typhoon claimed over 300 lives, and inflicted over US $3.3 billion in damage to agriculture—impacting farmland, factories, and infrastructure. In Thailand, northern provinces experienced the worst flooding of the century, so far: more than 150,000 families affected, at least 46 deaths, and damages estimated at US $812 million in Chiang Rai alone.

The rising cadence of extreme weather events—from deadly floods to persistent droughts around the world—has strengthened the investment case for geoengineering technologies that can avoid too much rainfall or bring back rainfall to regions left arid by global warming.

Over the past few months, we’ve connected with both individual & institutional investors in the space, here is what we’ve learned.

This investment research paper outlines the landscape, emerging opportunities, institutional allocations, risks, and clear entry points for forward-thinking capital allocators.

Geo-engineering vs. Planetary Health: Competing Paths for Global Resilience

With the success of the Star Wars Andor TV series, I couldn’t resist invoking a Star Wars metaphor to explain the pivotal choice we face in the future of Earth’s infrastructure.

We now stand at a planetary crossroads. Our generation decides if it’s green or steel.

On one side lies the Coruscant model—a vision of resilience built entirely through human engineering. In this future, we construct planetary life-support systems through vast cloud-seeding networks, stratospheric aerosol dispersal, desalination megaprojects, synthetic food systems, and bioengineered ecosystems. Much like Coruscant, the planet-wide city in Star Wars, this model is sleek, advanced, and completely divorced from the natural world beneath it. But it comes at a cost: resilience in this paradigm is artificial, energy-intensive, and requires constant capital injection to maintain equilibrium. It turns Earth into a climate-managed machine—capable of sustaining life, but only through relentless intervention and tightly centralized governance.

This is geoengineering as a defensive strategy—necessary in some contexts, but structurally fragile and fundamentally extractive.

On the other side is the Gaia model—a planetary infrastructure strategy based on restoring Earth’s innate systems: reforested watersheds, revived wetlands and mangroves, rebuilt topsoil, protected oceans, biodiversity corridors, and the return of keystone species. Rather than override nature, this approach reboots it. It draws on millions of years of evolutionary wisdom to build emergent resilience. Water is retained by forests, temperature moderated by healthy soils, carbon drawn down by algae and peat. It’s decentralized, lower-cost over time, and shock-resistant—because the system knows how to heal itself.

This model aligns with investments in planetary health: regenerative agriculture, biodiversity credits, blue carbon markets, and decentralized ecosystem restoration. Unlike geoengineering, it scales through communities, not just corporations.

The real challenge—and opportunity—for investors is not to pick one side, but to understand how these models interact. The Coruscant model might be needed to buy time. But the Gaia model is what lets us stay here.

For institutional investors, this is not a theoretical debate but a practical allocation decision. The next decade will dictate trillions in capital flows toward one of these two paths.

The Land Bottleneck — Why Wild Ecosystems Are The Primary Underpriced Asset

The recent buzz around de-extinction—like Colossal Biosciences’ woolly mammoth or CRISPR-ed dire-wolves—reflects a deeper misconception about the climate and biodiversity crisis.

Tech may revive species, but where will they live? Editing DNA doesn’t restore lost ecosystems. A mammoth without permafrost, or a bird without migratory corridors, is a spectacle—not a solution.

The real problem isn’t just extinction. It’s that we’ve destroyed natural systems that stored carbon and supported life—and we’ve also released ancient carbon reserves once buried safely underground.

For centuries, we’ve already been geo-engineering the planet in two ways:

By eliminating ecosystems that absorb carbon—old-growth forests, peatlands, wetlands, and oceans.

By unlocking fossil carbon—burning coal, oil, and gas created from ancient biomass, including plants and dinosaurs.

Today, we convert over 10 million hectares of forest annually—roughly Iceland’s size—into farmland, suburbs, and infrastructure. This not only emits carbon, it erases nature’s ability to absorb it. This is our passive geo-engineering.

Extinction and climate collapse unfold slowly: fragmented habitats, noise pollution, invasive species, ecological disconnection. The result? “Green deserts”—landscapes that look alive, but are biologically silent and incapable of supporting even a resurrected species.

The real challenge isn’t reviving species—it’s reviving the systems that let carbon and life flow naturally. It is to take control of our Geo-engineering footptint.

To understand these geo-engineering concepts—and its relationship to planetary health—we spoke with Jim Fournier, a single family office owner who’s been quietly investing in the space for nearly two decades.

His insights reveal how the sector has evolved from fringe academic theory into a serious pillar of the climate adaptation playbook.

From early marine cloud brightening trials to biomass-driven ocean alkalinity experiments, Jim’s portfolio reflects a future in which atmospheric engineering and ecological rebalancing are no longer in opposition—but co-evolving strategies.

The context is sobering: 72% of Earth’s terrestrial land surface is now under direct human influence, with agriculture alone consuming 40% of that land. In the U.S., only 14% of land is under any formal protection—and much of that is high-altitude desert or ecologically marginal terrain. In biodiversity-rich regions like Southeast Asia and sub-Saharan Africa, infrastructure sprawl and debt-fueled monoculture farming are accelerating the collapse of ecological integrity.

The question isn’t whether we should intervene in nature. We already have—on a planetary scale. The real question is: will we take responsibility of our footprint, will out next interventions regenerate nature or completely remove it?

The 25-Year Window for Adaptation Capital

By 2050, the global population will peak around 9.5 billion, with over 70% urbanized. Demographic shifts will simultaneously elevate global demands for food, energy, water, and infrastructure, just as climate-driven disruptions intensify. After this peak, demographic contraction and aging populations will shift global economic priorities from growth to resilience.

Without preemptively restoring planetary ecosystem functions—including stable oxygen production, freshwater security, fertile soils, and intact biodiversity networks—the underlying economic fabric will become profoundly fragile. Therefore, capital allocation toward ecosystem restoration today offers critical resilience and economic outperformance opportunities as scarcity-pricing and ecosystem service markets rapidly mature.

State of Capital Flows — Where Money Is Moving

As of early 2025, total institutional capital deployed into geoengineering-linked investments—including climate intervention technologies, atmospheric manipulation, and engineered carbon removal—is estimated at $50–75 billion, with forecasts to surpass $200 billion by 2027. This surge is driven by sovereign funds, corporates, and climate-forward family offices seeking long-duration, high-impact resilience strategies.

Key players in the emerging geoengineering investment ecosystem include:

Breakthrough Energy Ventures

Backed by Bill Gates and institutional LPs

Invested in advanced carbon capture (e.g., Heirloom), direct air capture, and solar geoengineering R&D

Focus: hard science startups targeting climate tipping points

Lowercarbon Capital

$1+ billion raised across climate deeptech funds

Portfolio includes Make Sunsets (stratospheric aerosol particles) and CarbonBuilt

Thesis: unapologetically funding moonshot approaches to “fix the air”

Prime Coalition

Non-profit catalytic capital platform supporting frontier climate tech

Focus areas: enhanced weathering, marine alkalinity, bio-geoengineering

LP base includes philanthropies and mission-driven institutions

Carbon Removal XPRIZE + Stripe Climate’s Frontier Fund

$1+ billion in advance purchase commitments for durable carbon removal

Supports technologies like ocean alkalinity (e.g., Captura, Running Tide) and mineralization

Funders include Stripe, Shopify, Meta, McKinsey, and Alphabet

These investors are shaping a new climate asset class—one that doesn’t just reduce emissions, but actively engineers planetary conditions. Unlike traditional ESG or mitigation-only approaches, this category bets on intervention, durability, and the convergence of biotech, energy systems, and atmospheric science.

Geo-Engineering Market Map — The First Movers

Always supporting you to stay ahead—Atlas Capital created this market map to help you understand, before the mainstream, how geo-engineering is rapidly evolving from fringe science to investable reality.

As the climate crisis reshapes risk, portfolios must adapt. From stratospheric aerosols to satellite-based ecosystem intelligence, these startups represent the early infrastructure of a new asset class we’ve called: Geo-Engineering & Planetary Health.

This market map is designed to help forward-thinking investors diversify into this new sector:

A new generation of startups is emerging at the intersection of atmospheric intervention and biodiversity regeneration. This map highlights key players across the geo-engineering landscape—from cloud seeding and direct air capture to ocean alkalinity, reforestation, and AI-powered planetary monitoring.

Hard geo-engineering ventures like Make Sunsets and Selerys are testing stratospheric aerosols and cloud ionization to manipulate local climate conditions.

In the oceans, companies like Captura and Ebb Carbon are pioneering ocean alkalinity enhancement and carbon drawdown at gigaton scale.

Land-based biome engineers such as Airbuild and AtmoCooling are reshaping built environments and microclimates through passive and active cooling tech.

Meanwhile, Mast Reforestation and Terraformation are rebuilding biodiversity at scale, often with drone-planting and carbon-linked financing.

AI and satellite monitoring like Albedo, AlphaGeo, and EarthDaily provide the planetary intelligence backbone needed to measure, monitor, and manage geo-engineering interventions in real time.

Together, these startups represent the emerging infrastructure of planetary health—where climate adaptation meets frontier tech and where atmospheric intervention becomes a new investment thesis.

Portfolio Construction for Family Offices & Angel Investors

As the geo-engineering and planetary health sectors evolve from fringe to institutional, forward-thinking family offices are allocating capital across a diversified basket of emerging infrastructure themes.

Sophisticated allocators deploying $10–100M are structuring climate portfolios as follows:

Land-Based Biome Engineering (20–40% allocation, targeting 12–18% IRR),

Ocean-Based Biome Engineering (10–20%, targeting 15–20% IRR),

Reforestation & Assets Re-Wilding (20–30%, mid-teens IRRs),

Planetary Health Solutions (10–20%, early-stage 5–10x return multiples),

Hard Geo-Engineering & Cloud Seeding, small allocations so far (<10%).

To support portfolio construction, Atlas Capital has created a model that offers curated access to top-tier general partners, vetted deal flow, and risk-managed exposure across these verticals. This structure provides family offices with institutional-grade diligence while preserving agility and thematic conviction.

Risk Factors and Mitigation Strategies

While the upside is significant, these frontier sectors come with their own set of structural risks:

Policy & Regulatory Uncertainty: Especially in geoengineering, biodiversity markets, and land-linked carbon claims

Sovereign Land Tenure Risk: Particularly in Southeast Asia, sub-Saharan Africa, and Latin America

Valuation Volatility & Liquidity Gaps: Early-stage biocredit exchanges are still developing pricing and clearing mechanisms

Mitigation Strategies Include:

Partnering only with institutional-grade GPs with on-the-ground presence

Diversified geographic exposures across political jurisdictions

Participation in structured co-investment vehicles (e.g. WeTheAtlas) with conservative underwriting

Complementing this capital strategy, this table illustrates how key institutional players like Temasek, and Brookfield are anchoring this transition. Their activity across marine and land-based geo-engineering signals the early formation of a resilient, high-growth potential asset class.

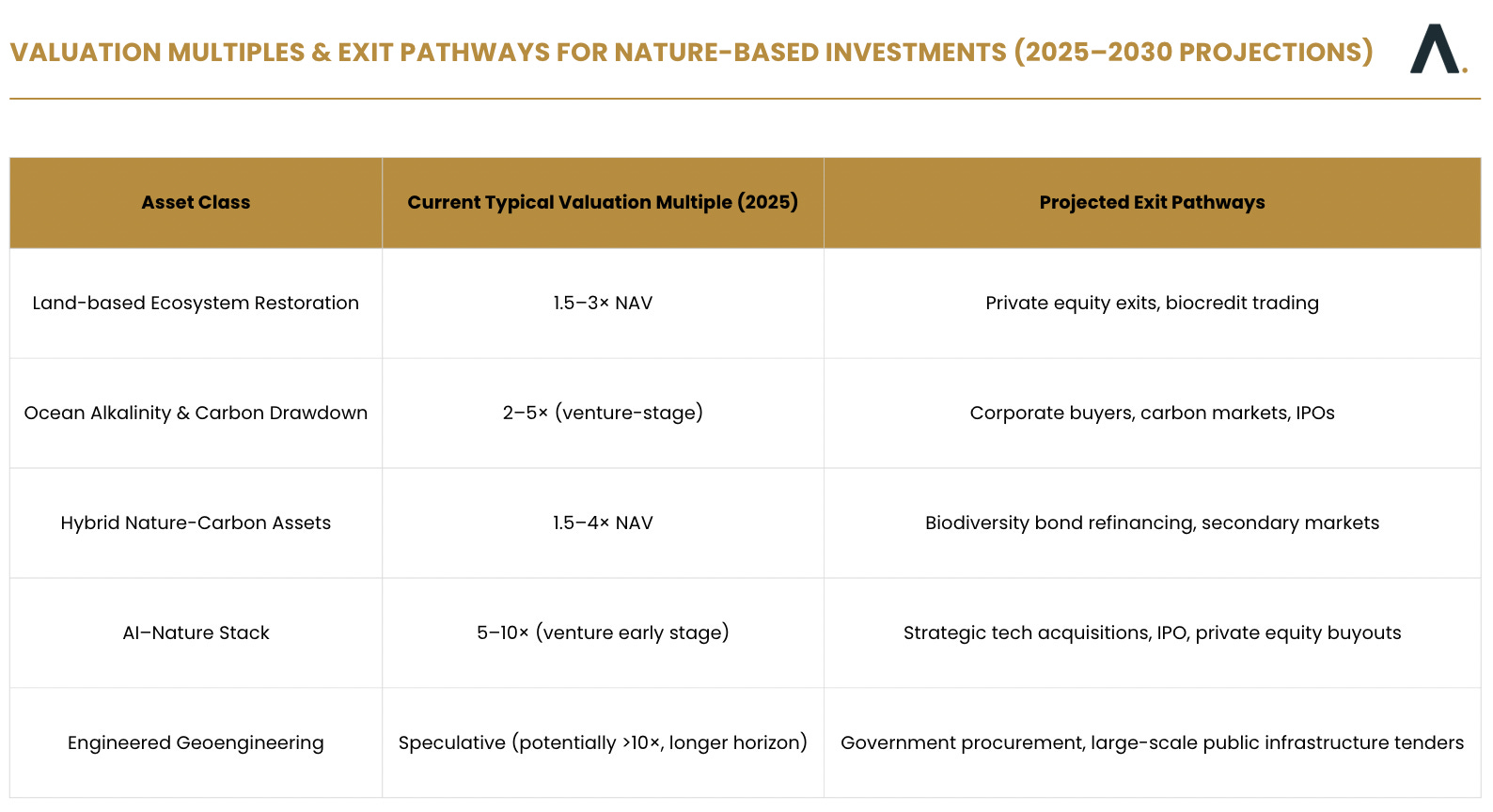

Valuation and Exit Pathways

This table highlights the increasingly viable exit landscape. In addition to private market appreciation, new liquidity options are emerging: geo-engineering & biodiversity linked sovereign bonds, income streams, secondary exchanges like CIX, and ETFs tracking capital in the space.

In short, planetary infrastructure is no longer just an environmental imperative—it’s an investment category with asymmetric upside and growing institutional alignment. For allocators seeking performance alongside planetary relevance, now is the time to build. Not after it’s already priced in.

Why Atlas Capital Holds a Strategic Edge

Atlas Capital uniquely positions investors ahead of mainstream capital flows through an adaptation-first investment thesis, proprietary pipeline via family office co-investment networks, frontier tech companies founders attending our conferences, and other general partners of prominent funds active in the space. This offers a critical first-mover advantage and foresight on what is bankable and what’s not.

Call to Action — Capitalizing on the Immediate Opportunity

The opportunity to capture asymmetric returns in Geo-engineering and Planetary Health is unfolding now—well before institutional capital fully saturates these markets.

Sign up for the waitlist of WeTheAtlas, our family office direct investing platform, to gain early access to open rounds already anchored by lead investors, and vetted listings of frontier deals for direct investing.

In the meantime, if you are interested to see some example of deals in the space that WeTheAtlas platform can provide, click here (Free)

Next Up — Biofuels for Marine Shipping & Logistics

In the next edition of The Adaptive Economy, we will deeply explore the investment landscape of Biofuels for Energy Resilience—an essential pillar of the new energy order— from biomethanol applied to marine shipping to biofuels & ammonia, as potential investments alongside large families actively deploying in the space.

Fight The Good Fight,

Djoann Fal